If your company imports goods from China or other countries targeted by U.S. trade enforcement actions, you've probably paid steep tariffs under Section 301. These duties—imposed in response to unfair trade practices—can add up to 25% or more on top of your landed cost. And for many businesses, those costs hit the bottom line hard. But here's the good news: in many cases, you can get that money back.

Thanks to the U.S. duty drawback program, importers and exporters may be eligible to recover up to 99% of the Section 301 tariffs they’ve paid—so long as the goods were later exported, used in manufacturing exports, or rejected and returned. This process is called a Section 301 duty drawback, and it can result in hundreds of thousands of dollars in recovered duties for qualifying businesses. Yet most companies still aren’t filing—often because they assume 301 duties aren’t eligible or the process is too complex.

In reality, Section 301 tariffs are eligible for drawback, and the process—while technical—can be made far easier with the right knowledge, tools, and support. U.S. Customs and Border Protection (CBP) has confirmed that duties paid under Section 301 are refundable under the Modernized Drawback regulations (19 CFR Part 190), provided the standard conditions for drawback are met.

That said, claiming duty drawback on Section 301 tariffs isn’t something you can do overnight. It requires proper documentation, accurate matching of import and export data, and a clear understanding of how different drawback provisions apply—especially when it comes to substitution claims and HTS code classifications. For many businesses, the difference between a successful refund and a denied claim comes down to recordkeeping and compliance.

This guide breaks down everything you need to know about duty drawback on Section 301 tariffs—from eligibility rules and documentation requirements to how the filing process works and how to maximize your potential refunds. Whether you’re an importer, exporter, customs broker, or 3PL partner, this article will help you understand how to recover duties you may have already overpaid—and avoid leaving money on the table.

Understanding Section 301 Tariffs

If you’ve ever looked at a customs duty statement and noticed a staggering charge labeled “301,” you’re not alone. Section 301 tariffs have become one of the most consequential trade enforcement tools used by the United States in recent years—and they continue to impact a wide range of industries.

Section 301 of the Trade Act of 1974 gives the U.S. Trade Representative (USTR) the authority to investigate and respond to unfair trade practices by other countries. In 2018, following an investigation into China’s intellectual property and technology transfer policies, the USTR imposed a sweeping series of tariffs on Chinese-origin goods. These duties—commonly referred to as Section 301 tariffs—now apply to thousands of products across categories like electronics, machinery, apparel, automotive parts, and industrial components.

Depending on the product, Section 301 duties can range from 7.5% to 25%—on top of any regular Most Favored Nation (MFN) duties or fees like MPF and HMF. And unlike anti-dumping or countervailing duties, which are narrowly targeted, Section 301 applies to broad categories of goods based on their Harmonized Tariff Schedule (HTS) classification.

The list of products subject to Section 301 tariffs has been rolled out in tranches—known as Lists 1 through 4—each covering different sets of HTS codes. Although some exclusions have been granted over time, many of the original tariffs remain in effect, and in some cases have been extended or modified. As of 2024, most goods on Lists 1, 2, and 3 are still subject to additional duties unless explicitly excluded.

For importers, these tariffs have had a lasting impact on landed costs, sourcing decisions, and margin pressure. And while some companies have shifted their supply chains outside of China to avoid these duties altogether, others—especially those in specialized manufacturing or electronics—simply can’t. For these businesses, recovering Section 301 tariffs through duty drawback has become a critical cost-recovery strategy.

Understanding where Section 301 duties come from—and why they still matter—is the first step toward navigating the recovery process. In the next section, we’ll explore how the duty drawback program works, and more importantly, how it applies specifically to Section 301 tariffs.

Can You Recover Section 301 Tariffs Through Duty Drawback?

The short answer is yes—Section 301 duties are eligible for drawback. But as with most things in trade compliance, the long answer is more nuanced. To successfully claim a duty drawback on Section 301 tariffs, you’ll need to meet several conditions laid out by U.S. Customs and Border Protection (CBP), and you’ll need the right documentation to prove it.

Section 301 Duties Are Legally Eligible for Drawback

Some importers mistakenly believe that Section 301 tariffs—because they are punitive in nature—are non-refundable. That’s not true. CBP has explicitly confirmed that duties imposed under Section 301 of the Trade Act of 1974 can be recovered through the federal drawback program, governed under 19 CFR Part 190 (Modernized Drawback). In other words, you can get up to 99% of your Section 301 duties back if the right conditions are met.

This eligibility applies across the three major drawback provisions. See our article "Types of Duty Drawback" for more information:

- Unused merchandise drawback (when imported goods are exported without being substantially changed)

- Manufacturing drawback (when imported materials are used in exported finished goods)

- Rejected merchandise drawback (when goods are returned or destroyed due to defect or non-conformance)

The key requirement is that the imported goods—or their derivatives—must leave the U.S. via export or be destroyed under CBP supervision. Simply selling the goods domestically, even at a loss, doesn’t qualify.

Substitution Drawback and Section 301 Duties

One of the most powerful tools in the drawback system is substitution drawback, which allows you to claim refunds based on commercially interchangeable goods—even if the exact imported item wasn’t exported. For many companies, this opens the door to recovering Section 301 duties even when inventory is pooled or fungible.

Substitution is allowed under 19 CFR § 190.22(a), but there’s a catch: the substituted export must share the same 8-digit HTS code as the original import. This rule is strictly enforced in Section 301 claims. If your HTS classifications aren’t consistent—or if you can’t match imports and exports at the 8-digit level—your claim could be denied.

Because Section 301 duties are tied directly to HTS codes (via Lists 1–4), substitution claims must be backed by clean, traceable data showing that the exported goods are commercially interchangeable with the dutiable imports. In practice, this usually means your products need to have a clearly documented Bill of Materials (BOM) or serial/lot tracking system in place—or a robust platform that can automate this matching process for you.

Time Limits Apply—Don’t Wait Too Long

Section 301 drawback claims are subject to the same general 5-year statute of limitations that applies to most duty drawback filings. The clock starts ticking from the date of import, not the date of export or filing. That means any eligible 301-duty-paid imports from 2019–2020 may already be outside the claim window unless you’ve already filed or preserved your rights.

To make matters more urgent, many companies that began paying steep 301 duties in 2020 are now reaching the outer limit of their recovery period. If you haven’t yet started your Section 301 duty drawback program, now is the time to act.

Don’t Let Confusion Stop You From Filing

Despite the clear legal basis, many companies still hesitate to file. They’re unsure if their records are complete enough. They don’t know which provision applies. Or they’re just overwhelmed by the idea of managing one more layer of compliance.

But inaction has a cost. Every month you delay could mean forfeiting tens—or even hundreds—of thousands of dollars in refundable duties. And with the right systems in place, filing a Section 301 duty drawback claim doesn’t have to be hard. In the next section, we’ll walk through how the process works from start to finish.

How the Section 301 Duty Drawback Process Works

Once you’ve confirmed that your company is eligible, the next step is navigating the actual Section 301 duty drawback filing process. While the fundamentals of filing are the same as any other type of drawback claim, 301 claims require a higher degree of accuracy—especially when it comes to matching imports and exports, classifying HTS codes, and complying with substitution rules.

Here’s how the process works, from import to refund.

Step 1: Identify Eligible Imports and Exports

The process begins by reviewing your import records for goods that were subject to Section 301 tariffs—specifically those with HTS codes listed on USTR Lists 1 through 4. These products are typically sourced from China and will have additional 301 duties reflected on your CBP Form 7501 (Entry Summary).

Next, identify which portion of those imports were later:

- Exported in the same condition or destroyed under CBP guidelines without being used (unused merchandise)

- Used in manufacturing goods that were exported (manufacturing drawback)

- Returned to supplier or destroyed (rejected merchandise)

Only these qualify for drawback. If the goods were sold domestically or used in internal operations, you can’t claim a refund.

Step 2: Match Imports to Exports

This is the most critical—and often the most time-consuming—part of the process. CBP requires clear evidence linking the imported goods (where duties were paid) to the exported goods (which trigger the refund). Depending on your drawback provision, this matching can be done through:

- Direct Identification, using serial numbers, lot numbers, or production logs

- Substitution, if the exported item shares the same 8-digit HTS code and is commercially interchangeable with the import

For Section 301 claims, substitution is especially powerful—but only if your records are clean and traceable. That’s why many companies rely on automated software to extract, clean, and match import/export data without relying on spreadsheets or manual workflows.

Step 3: Prepare the Documentation

Once import/export pairs have been identified, you’ll need to gather and prepare the core documents required by CBP. These include:

- CBP Form 7501 – showing payment of Section 301 duties

- Commercial invoices – for both imports and exports

- Bills of lading / Air waybills – proving physical export of goods

- HTS classification records – confirming 8-digit HTS match

- Inventory or production logs – showing traceability (especially for manufacturing claims)

- Waiver of drawback rights – if you’re not the importer or exporter of record

For each transaction, the documentation must clearly demonstrate the flow of goods: where they were imported, how they were handled, and when they left the country.

Step 4: File Through the ACE Portal

Once all documentation is organized, Section 301 duty drawback claims must be filed electronically through ACE (Automated Commercial Environment), the digital system managed by U.S. Customs and Border Protection (CBP).

To file a drawback claim through ACE, you’ll need to submit CBP Form 7551 along with all required supporting documents. If you’re requesting accelerated payment—where CBP issues a refund before full liquidation—you’ll also need a drawback bond that covers the value of the claim.

Only firms with ABI (Automated Broker Interface) certification are authorized to submit drawback claims directly to CBP. There are currently fewer than 30 ABI-certified drawback filers, including Pax AI, in the U.S., so most companies rely on a licensed broker, drawback specialist, or technology provider to file on their behalf.

Step 5: Wait for CBP Review and Refund

Once filed, CBP will perform a desk review. If everything checks out, and you’ve applied for Accelerated Payment privileges, you can expect to receive your 301 duty drawback refund in 30–45 days. Without accelerated payment, your refund will only be issued after full liquidation—an audit process that can take 1 to 4 years.

CBP may request additional documentation or clarification during their review, especially for large or high-risk claims. Keeping your records organized and audit-ready is essential.

Bottom Line: Process Matters

The Section 301 duty drawback process isn’t overly complicated—but it is meticulous. Small errors in HTS classification, mismatched records, or missing privilege applications can delay or derail your claim. That’s why companies recovering serious money from Section 301 tariffs are investing in structured processes, automated tools, and compliance-focused support to get it right the first time.

In the next section, we’ll dive deeper into who can file a Section 301 drawback claim—and what you need to do to qualify.

Who Can File—and What You Need to Be Eligible

Not every company that touches imported goods can automatically file for duty drawback. But the rules are more flexible than most businesses realize. In the case of Section 301 duty drawback, what matters is not just who paid the duty, but who has the legal right to claim a refund—and the documentation to prove it.

Importers, Exporters, and Manufacturers Can All File

The most common filer is the importer of record, since they’re the ones who paid the Section 301 tariffs at the time of entry. But they’re not the only ones who can file. In fact, if you’re an exporter, a contract manufacturer, or a 3PL (third-party logistics provider) involved in the movement or transformation of dutiable goods, you may still be eligible to recover those duties—if certain conditions are met.

CBP allows any party in the supply chain to file a drawback claim as long as they can demonstrate:

- Legal ownership or drawback rights to the imported goods

- Sufficient documentation to trace the import to the export (or destruction)

- Compliance with the correct drawback provision (e.g. unused, manufacturing, rejected)

Transferring Drawback Rights

If your company wasn’t the original importer of record, you can still file by obtaining a waiver of drawback rights from the importer. This is a standard legal document that assigns the right to claim a refund to another party—usually the exporter or manufacturer. These transfers are especially common in contract manufacturing and 3PL arrangements, where the party best positioned to file isn’t the one who paid the duties.

Similarly, if you’re the exporter but someone else handled the import, you can still be the claimant—so long as you have written authorization and access to the necessary documentation.

You’ll Need to Maintain Proper Records

Regardless of where you sit in the supply chain, CBP will expect you to provide full traceability between the dutiable import and the qualifying export or destruction. That means invoices, entry summaries, HTS codes, bills of lading, production logs, and anything else needed to verify that the goods were eligible and handled in compliance with the rules.

For Section 301 tariff drawback, this often includes proving that the exported goods either match the imported item exactly or meet the substitution criteria at the 8-digit HTS level. Without this documentation, even eligible claims may be denied.

Maximizing Your Refund: Common Strategies

Once you’ve established eligibility, the next step is making the most of it. Companies that file regularly and recover significant refunds on Section 301 duties don’t just meet the minimum requirements—they use every available strategy to increase the size and speed of their refunds. Here’s how they do it.

Apply for Drawback Privileges Early

One of the most effective ways to maximize your duty drawback program is by applying for drawback privileges with CBP. These are formal approvals that allow claimants to streamline the process and get paid faster.

There are three core types of privileges:

- Accelerated Payment – allows you to receive your refund within 30–45 days of filing, instead of waiting 1–4 years for liquidation

- Waiver of Prior Notice – lets you export goods without notifying CBP five days in advance

- Manufacturing Ruling – required for manufacturing drawback claims and can be general or specific

Without these privileges, even a valid Section 301 claim can get stuck in CBP’s audit queue for years. With them, your cash flow improves—and your program becomes more scalable over time.

Use Substitution Where Possible

If your imports and exports share the same 8-digit HTS code and are commercially interchangeable, substitution drawback can unlock far more recovery potential. Instead of tracking every individual product from import to export, you can pool fungible goods and file claims based on aggregated volumes.

For many companies—especially those dealing in high-volume, serialized, or commoditized inventory—substitution makes the difference between a one-time claim and a continuous refund pipeline. Just be sure your HTS classifications are accurate, consistent, and well-documented.

File Regularly, Not Just Retroactively

Duty drawback allows you to claim refunds on past imports going back up to five years—but the most efficient programs are proactive, not reactive. Companies that file quarterly or monthly tend to capture more eligible refunds, maintain cleaner documentation, and face fewer compliance issues during CBP review.

Waiting to file once a year—or worse, once every few years—leaves money on the table and increases the risk of lost records or missed timelines.

Automate Data Matching and Recordkeeping

Manual matching of imports to exports can work for small volumes, but for any business operating at scale, automation is key. Using AI-powered tools or integrated platforms to extract, match, and track your import/export data reduces human error and accelerates claim preparation.

It also creates a more reliable audit trail, helping you respond quickly to CBP inquiries and maintain eligibility for accelerated payment.

Filing Mistakes to Avoid

Even though Section 301 duties are eligible for drawback, not every claim results in a refund. Many companies lose out on recoverable duties simply because of avoidable errors—missing documentation, bad data, or filing too late. If you want your 301 duty drawback program to succeed, avoiding these common mistakes is just as important as following best practices.

Missing the 5-Year Deadline

One of the most common pitfalls is waiting too long to file. CBP’s drawback statute has a strict five-year limit from the date of importation—not the date of export or sale. That means if you imported dutiable goods in 2020 and haven’t filed a claim yet, you’re rapidly approaching (or may have already passed) the expiration window.

It’s not uncommon for companies to realize this too late, especially if they’re relying on spreadsheets or haven’t centralized their trade data. Once the five-year window closes, that refund is gone for good.

Poor Documentation or Inventory Traceability

CBP doesn’t just need to know that you paid Section 301 duties—they need to see how the imported goods were handled, what happened to them, and when they exited the country or were destroyed. If your documentation is inconsistent, incomplete, or lacks clear identifiers (like HTS codes, invoice numbers, or bill of lading references), your claim may be flagged for additional scrutiny—or outright denial.

This is especially risky in substitution drawback claims. If you’re filing based on commercial interchangeability, but can’t clearly show HTS code consistency across imports and exports, CBP may reject the claim or reduce the eligible refund amount.

Filing Without Drawback Privileges

It’s technically possible to file duty drawback without any formal privileges—but it’s rarely advisable. Without Accelerated Payment privileges, for example, you could be waiting years for your refund. And without a Waiver of Prior Notice, your exports must be pre-approved by CBP to qualify for drawback, creating delays and added complexity.

Many companies skip this step early on, not realizing how critical these privileges become once volume increases or audits begin. Filing without them often means more back-and-forth with CBP and slower refund timelines.

Using the Wrong HTS Code or Provision

Another common issue is applying the wrong drawback provision or misclassifying products under the wrong HTS code. Because Section 301 duties are tied directly to HTS classifications (based on Lists 1–4), errors here can lead to disallowed claims.

This is especially important for companies using substitution. If your export doesn't match the imported item at the 8-digit HTS level, even if the products are nearly identical, you may not be able to file under 301. A single digit can make or break a claim.

How Much Can You Recover?

If you’ve been paying Section 301 tariffs for years, the natural question is: How much of that money can you get back? The answer depends on your import volumes, your export activity, and how well your documentation supports a clean claim. But in many cases, the refund amount is substantial—especially for companies with ongoing exposure to China-origin goods.

Duty Drawback on Section 301 Tariffs: Up to 99% Recovery

Under U.S. law, duty drawback allows claimants to recover up to 99% of duties, taxes, and fees paid on imported goods—Section 301 tariffs included. This is not a partial rebate or tax credit. If your goods meet the eligibility requirements, the refund is nearly total.

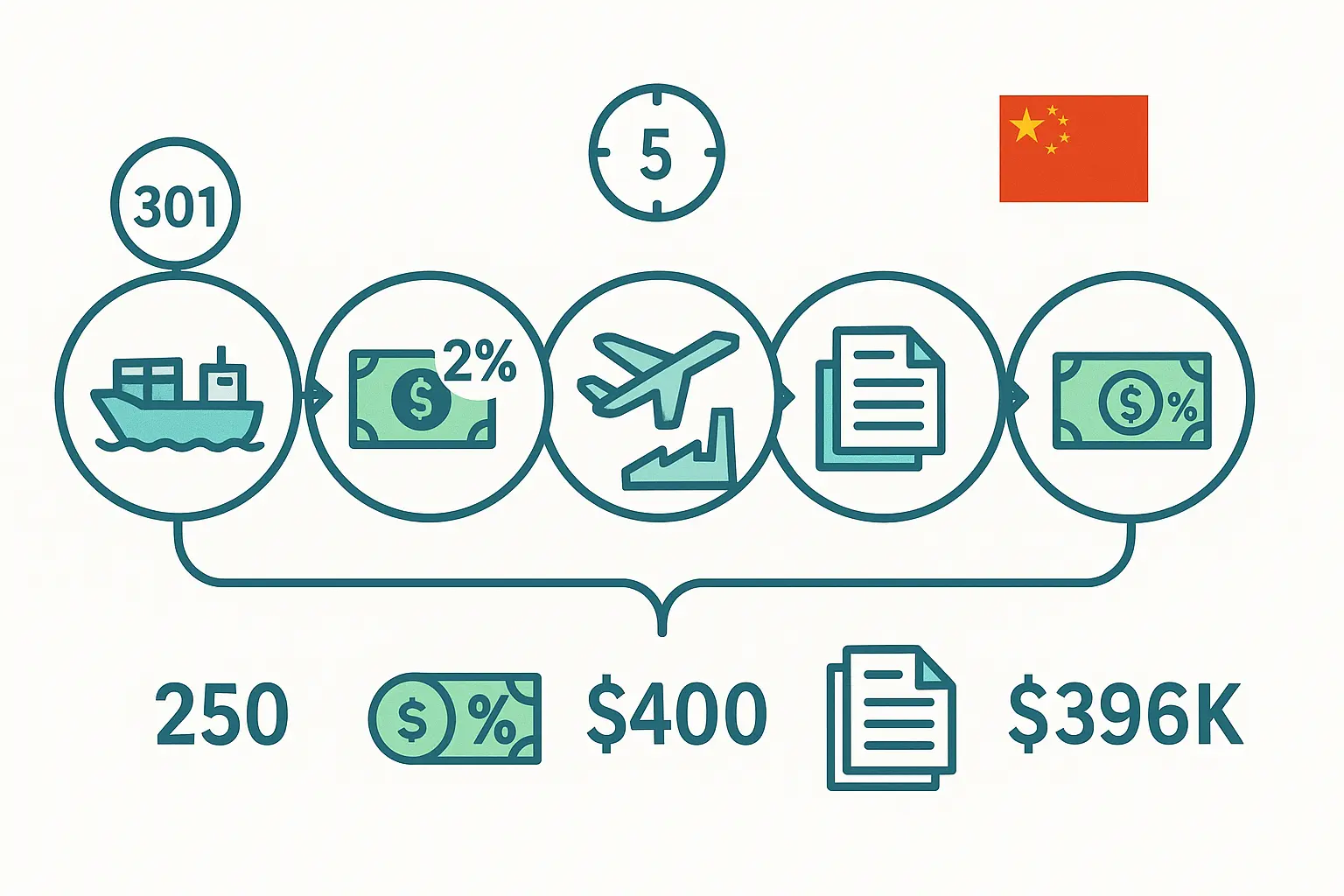

For example, if your company imported $2 million in electronics components from China and paid an additional $400,000 in Section 301 tariffs, you could be eligible to recover up to $396,000—assuming those goods (or interchangeable substitutes) were exported, destroyed, or used in exported manufacturing.

Refund Potential Varies by Industry

While exact amounts vary, here are a few illustrative cases drawn from across industries:

- A mid-sized apparel brand that shifted most of its supply chain to Asia recovered over six figures in refunds within the first year of filing.

- A medical device importer shipping to Latin America recouped tens of thousands in previously untapped 301 duties on unused merchandise exports.

- An industrial component supplier using substitution matched U.S. exports against pooled imports and established a recurring quarterly refund program.

These companies aren’t outliers—they’re simply acting on a program that many businesses overlook or underestimate.

Estimating Your Refund Potential

A quick way to estimate your refund opportunity is to multiply your total Section 301 duties paid over the past five years by the percentage of those goods that were exported, used in exports, or rejected:

Refund = Section 301 duties × % of qualifying exports × 99%

The tricky part is determining what portion of your imports actually qualify—which is where having access to clean import/export data and automated matching tools becomes essential.

Don’t Wait Too Long to Act

Because of the 5-year limit from the date of import, your window to recover older 301 duties is closing fast. Many companies that began paying steep tariffs in 2019 or 2020 are now at risk of losing those refunds permanently. Even if your documentation is messy, there may still be time to file—especially with help from a broker or drawback technology partner.

Filing Section 301 Drawback with Pax AI

Filing a Section 301 duty drawback claim requires precision—clean records, accurate matching, and full compliance with U.S. Customs regulations. For many companies, the challenge isn’t just figuring out whether they qualify—it’s figuring out how to manage the process at scale, without relying on manual work or fragmented systems.

That’s where Pax AI comes in. We combine licensed human expertise with powerful automation to simplify and streamline the entire drawback process—from onboarding to refund.

AI-Powered Import/Export Matching

One of the hardest parts of filing a 301 duty drawback claim is matching imports and exports across multiple years of trade data. Pax’s duty drawback platform automatically scans and links commercial invoices, entry summaries (CBP 7501), bills of lading, and export docs—identifying refund-eligible transactions with over 90% accuracy.

Whether you’re filing under direct identification or substitution, the platform ensures each claim is backed by compliant, traceable records—and flags anything that needs manual review before filing.

Best-in-Class Refund Optimization

Beyond compliance and automation, Pax’s platform is also built to maximize your refund, not just process it. Our optimization algorithm built by MIT mathematicians analyzes historical data, tariff rates, HTS performance, and export timing to help clients recover up to 15% more than they might through traditional brokers or manual filing.

That includes identifying and mathematically optimizing for:

- Missed substitution opportunities across pooled inventory

- Underutilized export records tied to eligible imports

- Filing strategies that better align with HTS classifications and seasonal trends

In other words, we don’t just help you get your money back—we help you get more of it. For clients dealing with complex supply chains or high duty exposure under Section 301, this difference can translate to hundreds of thousands in recovered revenue over time.

Direct Filing with CBP

Pax is one of fewer than 30 ABI-certified drawback filers in the U.S., which means we file claims directly to U.S. Customs through the ACE system—no middlemen, no delays. This also allows us to track claims in real time and quickly respond to any CBP inquiries. Every filing is reviewed by a licensed customs broker before submission to ensure accuracy and compliance.

Audit-Ready Recordkeeping

All submitted claims and supporting documentation are archived in a centralized dashboard—searchable, exportable, and ready for audit at any time. If CBP requests clarification, Pax clients can respond within hours, not weeks.

Accelerated Payment Support

If you haven’t yet applied for drawback privileges, Pax can handle that too. During onboarding, we help clients apply for accelerated payment, waiver of prior notice, and (if applicable) a manufacturing ruling—so you can get your refund in 30–45 days instead of waiting years.

Conclusion: Don’t Leave Your Section 301 Refunds on the Table

If your business has paid tariffs under Section 301—even years ago—there’s a good chance you’re eligible to get that money back. With duty drawback, you can recover up to 99% of those duties, turning what was once a sunk cost into real cash flow. And yes, Section 301 duties are fully eligible—as long as your exports, manufacturing, or rejections meet the criteria and are properly documented.

The process can be technical, but it doesn’t have to be painful. With the right data, systems, and partners in place, filing for Section 301 duty drawback can become a reliable, recurring refund strategy—not just a one-time recovery effort.

At Pax AI, our duty drawback company specializes in making that happen. Whether you’re just starting to explore drawback or already filing and want to recover more, we can help you simplify the process, ensure compliance, and maximize your refund.

Ready to find out what you could recover? Reach out for a quick estimate or onboarding walkthrough—we'll help you put your Section 301 duties to work.